How Stablecoins Are Creating Faster and Smarter Global Transactions

Global financial infrastructure is undergoing a structural transformation. For decades, international payments have depended on layered banking networks, delayed settlement cycles, currency conversion inefficiencies, and fragmented compliance systems. While digital banking improved accessibility, the core architecture behind cross-border settlement remained relatively slow and operationally expensive. Stablecoins are now changing that equation.

Unlike volatile cryptocurrencies, stablecoins are designed to maintain a consistent value by being pegged to fiat currencies or reserve-backed assets. This stability enables them to function as programmable digital cash within blockchain ecosystems. More importantly, they are introducing a new transaction model where settlement becomes faster, liquidity becomes more dynamic, and payment infrastructure becomes significantly more interoperable across markets.

As enterprises, fintech firms, and financial institutions look for frictionless payment rails, stablecoins are emerging as a foundational layer for next-generation global commerce.

The Limitations of Traditional Cross-Border Payment Systems

Traditional international payment systems rely heavily on intermediary banking networks. A transaction moving from one country to another often passes through multiple correspondent banks before final settlement occurs. Each intermediary introduces additional fees, reconciliation delays, compliance verification requirements, and operational dependencies.

Several structural inefficiencies continue to affect legacy systems:

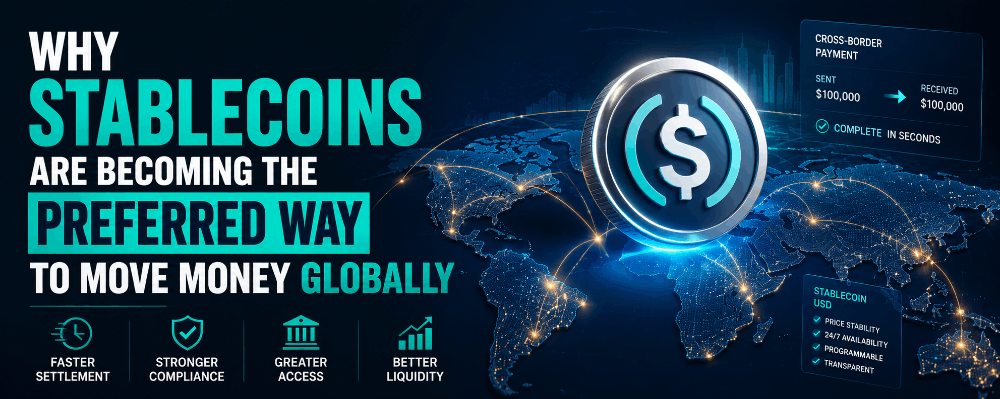

- Cross-border transfers may take several business days due to clearing and settlement procedures.

- Foreign exchange conversion introduces unpredictable pricing spreads.

- Payment tracking remains fragmented across institutions.

- Treasury management becomes difficult for multinational enterprises operating in multiple currencies.

- Banking cut-off times and regional holidays delay liquidity movement.

These inefficiencies are especially problematic in high-volume industries such as e-commerce, remittance processing, international payroll, supply chain finance, and B2B settlements. Businesses operating across jurisdictions increasingly require real-time settlement infrastructure that functions continuously without dependency on banking windows.

Stablecoins address many of these constraints by enabling direct value transfer on blockchain networks with near-instant settlement capability.

How Stablecoins Enable Faster Transaction Settlement

The biggest operational advantage of stablecoins lies in settlement finality. Instead of relying on layered intermediaries, blockchain networks validate and record transactions through decentralized consensus mechanisms. This reduces the time required for transaction confirmation and minimizes reconciliation overhead.

When stablecoins are integrated into payment ecosystems, transactions can settle within minutes rather than days. The result is not only speed but also improved capital efficiency. Businesses no longer need to keep excessive idle liquidity parked across multiple banking corridors to compensate for settlement delays.

Stablecoin-powered payment infrastructure introduces several transformative capabilities:

- Continuous 24/7 transaction processing without banking hour restrictions.

- Real-time treasury visibility across distributed financial systems.

- Reduced intermediary dependency during international settlements.

- Faster supplier payouts and vendor reconciliation.

- Lower transaction costs in high-frequency payment environments.

This shift is particularly valuable for enterprises managing global operations. Modern financial institutions are increasingly exploring blockchain-based settlement layers and Enterprise Stablecoin Services to optimize internal treasury workflows, institutional settlements, and programmable payment automation.

As blockchain interoperability frameworks mature, stablecoins are evolving from crypto-native assets into enterprise-grade financial instruments capable of supporting regulated digital finance ecosystems.

The Rise of Programmable Payments and Smart Financial Automation

One of the most underestimated advantages of stablecoins is programmability. Traditional banking infrastructure processes payments as static transactions. Blockchain-based stablecoins, however, can integrate directly with smart contracts, enabling conditional transaction execution and automated financial workflows.

This creates an entirely new operational model for businesses.

For example, payments can be programmed to execute automatically once contractual conditions are met. Supply chain settlements can trigger instantly after shipment verification. Payroll systems can distribute funds globally through automated smart contract logic. Subscription platforms can process recurring settlements transparently without manual intervention.

This programmable architecture introduces several operational benefits:

- Automated compliance and transaction verification workflows.

- Smart escrow mechanisms for international trade settlements.

- Instant royalty distribution for digital asset ecosystems.

- Real-time invoice settlement in B2B environments.

- Transparent audit trails for financial reporting and governance.

The combination of blockchain transparency and stable asset valuation allows organizations to modernize payment operations without inheriting the volatility risks associated with traditional cryptocurrencies.

As financial systems increasingly adopt tokenized infrastructure, programmable stablecoin payments are expected to become integral to digital commerce, decentralized finance, and embedded financial ecosystems.

Stablecoins and Financial Inclusion in Emerging Markets

Stablecoins are also reshaping financial accessibility in regions with limited banking infrastructure. In many emerging economies, access to stable financial systems remains inconsistent due to inflation, currency instability, or underdeveloped banking networks.

Blockchain-based stablecoins offer an alternative mechanism for storing and transferring value digitally without requiring full dependence on domestic banking infrastructure. Individuals and businesses can transact globally using internet-connected devices while bypassing traditional settlement bottlenecks.

This creates meaningful opportunities in areas such as:

- Cross-border freelancer payments.

- International remittance transfers.

- SME trade settlements.

- Digital commerce expansion.

- Mobile-first financial services.

For small businesses operating internationally, stablecoins reduce dependence on expensive remittance channels and foreign exchange intermediaries. Settlement becomes faster, more transparent, and significantly more accessible.

In regions experiencing local currency depreciation, stablecoins also function as a hedge against inflation volatility. While regulatory oversight remains essential, the underlying utility of stable digital assets continues to attract institutional and commercial interest worldwide.

The growing integration of blockchain wallets, fintech applications, and digital identity systems further accelerates stablecoin adoption across underserved markets.

Regulatory Evolution and the Future of Global Stablecoin Transactions

Regulation will ultimately determine the pace and scale of stablecoin adoption. Governments and financial regulators are increasingly recognizing that stablecoins represent more than speculative crypto instruments. They are becoming part of broader digital payment modernization strategies.

Several jurisdictions are actively developing frameworks focused on:

- Reserve transparency requirements.

- Consumer protection standards.

- Anti-money laundering compliance.

- Transaction monitoring infrastructure.

- Licensing models for stablecoin issuers.

This regulatory evolution is important because institutional adoption depends heavily on compliance clarity. Enterprises require predictable governance structures before integrating stablecoin infrastructure into mission-critical financial operations.

At the same time, central banks are evaluating how stablecoins may coexist with central bank digital currencies (CBDCs) and tokenized banking systems. The future financial ecosystem may ultimately consist of interoperable digital assets operating across both public and permissioned blockchain environments.

What makes stablecoins particularly powerful is their ability to bridge traditional finance and decentralized infrastructure simultaneously. They retain the transactional familiarity of fiat currency while introducing the efficiency, automation, and interoperability of blockchain technology.

As global commerce becomes increasingly digital, businesses are prioritizing settlement systems that are faster, programmable, transparent, and operationally scalable. Stablecoins are rapidly positioning themselves at the center of that transformation.