How Payment-Focused Cryptocurrency Coins Are Competing With Traditional Banking Systems

The global financial ecosystem is undergoing a structural transformation as payment-focused cryptocurrency coins redefine how value is transferred, settled, and recorded. Unlike legacy banking rails that rely on centralized clearinghouses and multi-layered intermediaries, blockchain-based payment tokens operate on decentralized, consensus-driven infrastructures. This paradigm shift is not merely technological—it is economic, operational, and regulatory in scope.

As digital assets evolve, their competition with traditional banking systems intensifies, particularly in areas such as cross-border payments, transaction finality, and liquidity efficiency.

Decentralized Payment Architecture vs Centralized Banking Systems

Traditional banking systems are built on centralized ledgers, where financial institutions act as custodians, validators, and intermediaries. This model introduces latency due to clearing and settlement cycles, often governed by batch processing and jurisdictional compliance layers.

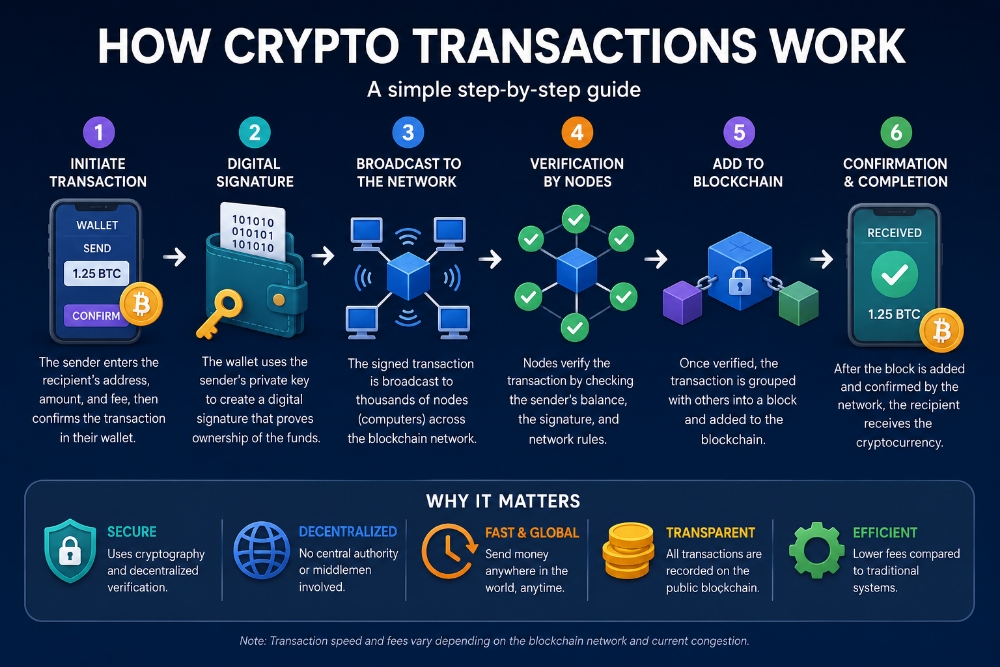

In contrast, payment-focused cryptocurrencies leverage distributed ledger technology (DLT), where transaction validation occurs via consensus mechanisms such as Proof-of-Stake (PoS) or Byzantine Fault Tolerance (BFT). This eliminates the need for correspondent banking networks and reduces systemic dependency on intermediaries.

Blockchain-based systems provide:

- Immutable transaction records secured through cryptographic hashing

- Peer-to-peer (P2P) transfer protocols eliminating third-party authorization

- Deterministic settlement with reduced counterparty risk

This architectural divergence enables cryptocurrencies to function as both a medium of exchange and a settlement layer, effectively collapsing the traditional multi-step banking workflow into a single atomic transaction.

Transaction Efficiency and Cost Optimization

One of the most significant competitive advantages of payment-focused cryptocurrency coins lies in transaction throughput and cost efficiency. Traditional banking infrastructures, particularly for cross-border remittances, involve multiple intermediaries, resulting in high fees and prolonged settlement times.

Key efficiency drivers include:

- Near-instant settlement cycles, often completed within seconds or minutes

- Elimination of intermediary fees, reducing transaction costs significantly

- 24/7 network availability, bypassing banking hours and holiday constraints

In conventional systems, international wire transfers can take several business days due to clearing processes and currency conversions. In contrast, blockchain-enabled payments operate on a continuous settlement model, enabling real-time liquidity transfer.

This efficiency is particularly impactful in high-volume B2B transactions and remittance corridors, where cost compression directly improves operational margins.

Transparency, Security, and Cryptographic Integrity

Security and transparency are foundational to the competitive positioning of cryptocurrency payment systems. Traditional banking databases are centralized, making them susceptible to single points of failure and cyber vulnerabilities.

Blockchain networks, however, utilize cryptographic primitives such as public-private key encryption and Merkle tree structures to ensure data integrity. Every transaction is recorded on a distributed ledger, providing full auditability and traceability.

Notable advantages include:

- Tamper-resistant transaction records stored across decentralized nodes

- Reduced fraud vectors due to cryptographic validation mechanisms

- Enhanced transparency through publicly verifiable ledgers

Additionally, the absence of sensitive personal data in transaction payloads reduces the risk of identity theft and data breaches.

This security model contrasts sharply with traditional banking systems, where data centralization increases exposure to systemic risks.

Financial Inclusion and Borderless Accessibility

Payment-focused cryptocurrency coins are also addressing structural inefficiencies in global financial inclusion. Traditional banking systems often exclude populations due to stringent KYC requirements, geographic limitations, and infrastructure constraints.

Blockchain-based payment systems enable permissionless access, allowing users to participate in financial networks with only a digital wallet and internet connectivity.

This creates several implications:

- Inclusion of unbanked and underbanked populations into global commerce

- Frictionless cross-border transactions without currency restrictions

- Reduced dependency on national financial infrastructures

The emergence of stablecoins and programmable payment layers further enhances usability by mitigating volatility while enabling automated settlement via smart contracts. This programmability introduces new financial primitives such as conditional payments and escrow automation.

Within this evolving ecosystem, the role of a cryptocurrency coin development company becomes increasingly relevant in designing scalable, payment-optimized blockchain architectures that align with enterprise-grade requirements.

Institutional Convergence and the Future of Payments

Despite the disruptive potential of cryptocurrencies, the competition with traditional banking is not purely adversarial. Increasingly, financial institutions are integrating blockchain-based payment solutions to enhance efficiency and remain competitive.

Recent developments indicate:

- Banks experimenting with blockchain-based settlement systems for real-time payments

- Growing institutional acceptance of stablecoins for faster and more transparent transactions

- Hybrid financial models combining traditional compliance frameworks with decentralized infrastructure

This convergence suggests that the future of payments may not involve outright displacement but rather the coexistence of decentralized and centralized systems. Cryptocurrencies act as an innovation layer, pushing traditional banking toward modernization while simultaneously filling gaps in efficiency and accessibility.

Conclusion

Payment-focused cryptocurrency coins are fundamentally reshaping the competitive dynamics of the financial sector. By offering decentralized validation, real-time settlement, reduced transaction costs, and enhanced security, they challenge the operational limitations of traditional banking systems.

However, the evolution of this competition is nuanced. While cryptocurrencies excel in efficiency and accessibility, traditional banks continue to dominate in regulatory compliance, consumer protection, and financial stability. The intersection of these systems is likely to define the next generation of global payment infrastructure—one that is faster, more transparent, and increasingly decentralized.