Title: How Blockchain Is Transforming Trust in the Digital World

Over the past decade, blockchain technology has evolved from a niche innovation into one of the most influential technologies shaping the future of the internet. Initially introduced through Bitcoin in 2009 by Satoshi Nakamoto, blockchain has expanded far beyond digital currency. Today, it is transforming industries such as finance, healthcare, supply chain, and digital identity by solving one of the internet’s biggest problems: trust.

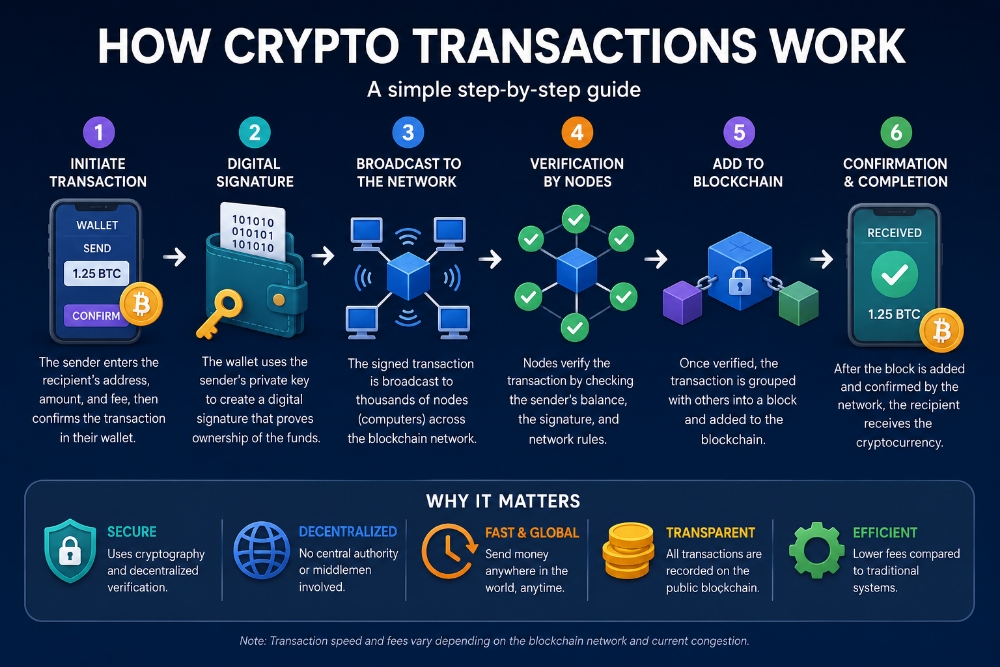

At its core, blockchain is a decentralized digital ledger that records transactions across a network of computers. Instead of relying on a central authority like a bank or government to verify transactions, blockchain uses cryptography and distributed consensus to ensure that records are accurate and tamper resistant. Once information is recorded on a blockchain, it becomes extremely difficult to change, making the system transparent and secure.

One of the most powerful aspects of blockchain technology is decentralization. Traditional systems rely on centralized intermediaries. For example, banks manage financial transactions, social media companies control user data, and governments maintain identity systems. While these centralized structures work, they also create single points of failure and control. Data breaches, corruption, censorship, and inefficiencies often arise when too much power is concentrated in one place.

Blockchain removes the need for these intermediaries by distributing control across a network. Every participant in the network has access to the same ledger, and transactions must be verified collectively. This shared system creates transparency and accountability while reducing the risk of manipulation.

Another major innovation enabled by blockchain is the concept of smart contracts. Smart contracts are self executing agreements written in code that automatically carry out actions when certain conditions are met. Platforms like Ethereum made smart contracts widely accessible, allowing developers to build decentralized applications that operate without human intervention.

For example, in a traditional contract, two parties might rely on lawyers, banks, or third parties to enforce an agreement. With a smart contract, the rules are programmed directly into the blockchain. If the conditions are satisfied, the contract executes automatically. This reduces costs, eliminates delays, and minimizes the risk of disputes.

Blockchain is also transforming supply chain management. Many companies struggle to track products accurately from the point of origin to the final consumer. Fraud, counterfeiting, and lack of transparency can create major problems in industries such as food production, pharmaceuticals, and luxury goods. By recording every step of a product’s journey on a blockchain, companies and consumers can verify authenticity and trace the origin of goods instantly.

In the financial sector, blockchain has introduced the concept of decentralized finance, often referred to as DeFi. DeFi platforms allow people to borrow, lend, trade, and earn interest on digital assets without traditional banks. Instead of relying on financial institutions, users interact directly with blockchain protocols. This creates new opportunities for financial inclusion, especially for individuals in regions where access to banking services is limited.

Another important use case for blockchain is digital identity. Millions of people around the world lack official identification, which limits their ability to access services such as banking, education, and healthcare. Blockchain based identity systems can provide individuals with secure, self controlled digital identities. Rather than storing personal information in centralized databases that can be hacked, blockchain allows individuals to control their own data while sharing only the information required for verification.

Despite its potential, blockchain technology still faces several challenges. Scalability remains a major issue, as some networks struggle to process large numbers of transactions quickly. Regulatory uncertainty also affects adoption, as governments and institutions work to understand how blockchain fits within existing legal frameworks. Additionally, energy consumption concerns have been raised about some blockchain networks, though newer technologies are being developed to address these issues.

Even with these challenges, the long term potential of blockchain remains enormous. As the internet continues to evolve toward a more decentralized model often called Web3, blockchain may serve as the foundation for a more open, transparent, and user controlled digital ecosystem.

In the coming years, blockchain could redefine how we exchange value, share information, and build trust online. Instead of relying on centralized institutions, individuals may increasingly rely on decentralized networks where transparency, security, and fairness are built directly into the technology itself.