Decentralized Lending Without Liquidity Pools, Custodians, or Smart Contract Middlemen

🏦 The Problem With “Decentralized” Lending

Decentralized finance was supposed to remove banks, custodians, and middlemen from lending.

In theory, that sounds simple:

A lender has money.

A borrower needs money.

Collateral protects the lender.

The blockchain enforces the rules.

But in practice, much of DeFi lending has not worked that way.

Many lending platforms that call themselves decentralized still depend on layers of infrastructure that are not truly peer-to-peer. Liquidity pools, governance contracts, price oracles, admin keys, liquidation bots, frontend operators, bridge dependencies, and protocol-controlled incentives often sit between the borrower and the lender.

That creates a strange contradiction.

The branding says decentralized lending.

The architecture often says platform-mediated lending.

Contractless loans were built from a different starting point.

Instead of building a lending platform on top of a blockchain, Contractless makes loans a native transaction type inside the blockchain itself.

That means loans are not just smart contracts deployed by a third party. They are part of the protocol.

⚠️ What Went Wrong With DeFi Lending?

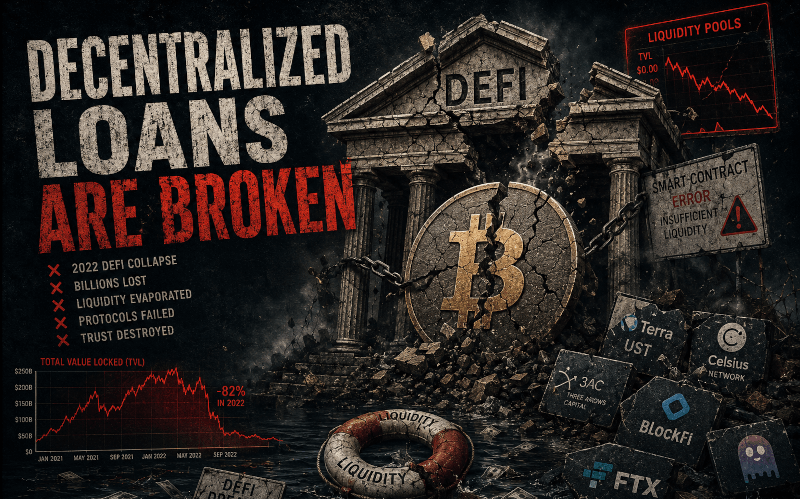

The 2022 crypto crash exposed a truth that many people already suspected: a lot of the lending ecosystem was more fragile than it appeared.

The collapse of Terra/Luna, the failure of major crypto lenders, the liquidation of Three Arrows Capital, and the bankruptcy or shutdown of firms like Celsius, Voyager, BlockFi, and others showed how deeply interconnected the market had become.

Some failures were centralized lenders pretending to be safer than they were. Others were DeFi mechanisms that depended on fragile assumptions: deep liquidity, stable collateral values, functioning liquidators, healthy markets, reliable oracles, and users not all running for the exit at the same time.

When those assumptions failed, the damage spread quickly.

A few common problems showed up again and again.

💧 Liquidity Pools Can Become a Weak Point

Most DeFi lending platforms are built around liquidity pools.

Users deposit assets into a pool. Borrowers borrow from that pool. Interest rates are determined by utilization. Liquidations are triggered when collateral ratios fall below certain thresholds.

That model can work, but it creates several risks:

- Lenders are often pooled together instead of making direct loan agreements.

- Borrowers do not always know or care who funded the loan.

- The health of the system depends on liquidity staying available.

- If too many people withdraw or too much collateral must be liquidated at once, the system can become unstable.

- Bad debt can affect the pool, not just one lender.

Liquidity pools are efficient, but they are not magic. They concentrate risk.

When markets are healthy, the pool looks deep and liquid.

When markets panic, liquidity can vanish exactly when it is needed most.

This is one reason DeFi liquidations can become violent. If a protocol must sell collateral into a falling market, liquidations can push prices lower, which triggers more liquidations, which pushes prices lower again.

That is how a lending mechanism can become a market-crashing mechanism.

🔥 Liquidation Cascades Are Not Theoretical

In crypto, collateral values can move fast.

If a lending protocol relies on automated liquidation, the system must answer a brutal question:

What happens when everyone becomes undercollateralized at once?

Many DeFi systems assume liquidators will step in, repay debt, collect collateral, and restore balance. But liquidators are profit-seeking actors. If liquidity is thin, gas fees are high, markets are moving too fast, or collateral is hard to sell, liquidations may not happen cleanly.

Sometimes they happen too aggressively.

Sometimes they do not happen fast enough.

Sometimes they create bad debt.

Sometimes they create price spirals.

This does not mean automated lending can never work. It means that lending protocols built around pools and liquidations are only as strong as their weakest market condition.

Contractless loans take a more direct approach.

🧩 Smart Contract Doesn't Mean Decentralization

Many DeFi loans are implemented through smart contracts.

That sounds decentralized, but the details matter.

A smart contract system may still depend on:

- Upgradeable contracts

- Admin permissions

- Governance votes

- External price oracles

- Liquidation bots

- Protocol-owned frontends

- Liquidity providers

- Incentive emissions

- Wrapped assets

- Bridges

- Centralized stablecoins

That is a lot of infrastructure for something that is supposed to be a loan.

The more moving pieces a system has, the more ways it can fail. Even when the contract code itself works as written, the system around it may not.

Contractless loans are designed around a much simpler question:

Can two parties create a loan directly, with the blockchain validating the terms natively?

The answer is yes.

🧱 What Are Contractless Loans?

Contractless loans are native decentralized loans built directly into the Contractless blockchain.

They are not smart contracts.

They are not liquidity pool positions.

They are not platform balances.

They are not promises made by a lending company.

They are blockchain-level transaction types.

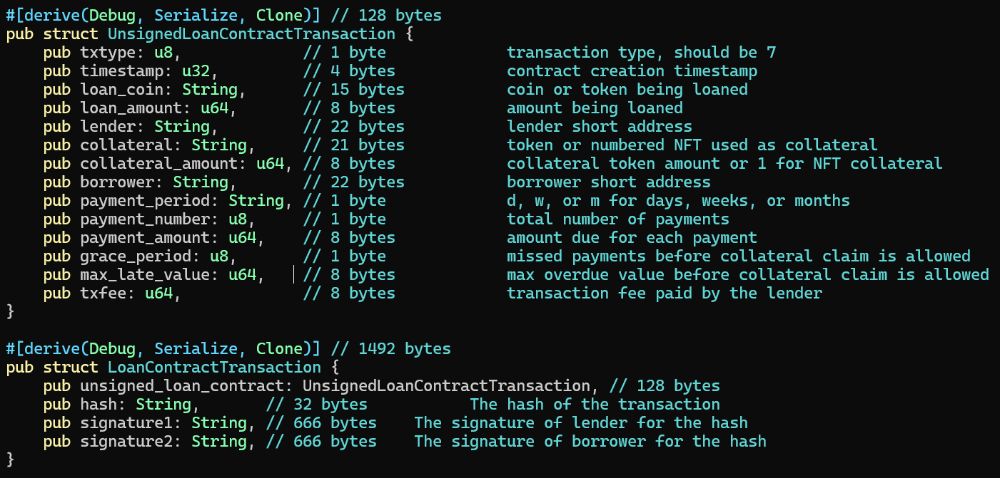

A Contractless loan involves three core transaction types:

- Create Loan

- Loan Payment

- Collateral Claim

Together, these allow a lender and borrower to create a loan, repay it over time, and enforce collateral rules if the borrower fails to meet the required conditions.

🤝 Peer-to-Peer Instead of Pool-to-User

The biggest difference is that Contractless loans are direct.

A lender agrees to lend a specific asset.

A borrower agrees to provide specific collateral.

Both parties sign the loan transaction.

The blockchain validates the transaction.

The loan terms are recorded directly on chain.

There is no liquidity pool between them.

That matters.

In a pool-based system, lenders often provide capital into a shared pool and borrowers draw from it. The lender is exposed to the health of the protocol and the pool.

In Contractless, the loan is between the actual lender and borrower. The rules are attached to that loan, not to a global pool.

This makes the risk easier to understand.

The lender is not asking, “Is this lending protocol solvent?”

The lender is asking, “Do I accept this borrower, this collateral, and these loan terms?”

That is much closer to how loans work in the real world.

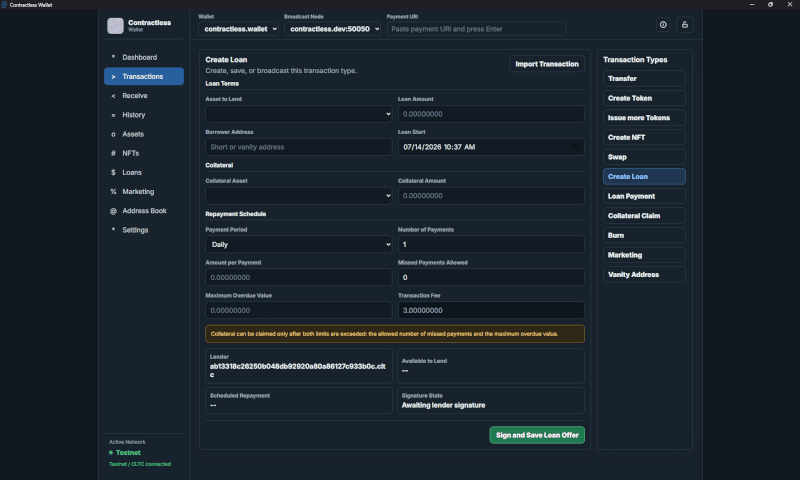

📜 How Contractless Loan Creation Works

A Contractless loan begins with a loan creation transaction.

The loan defines details such as:

- Lender

- Borrower

- Asset being loaned

- Amount being loaned

- Collateral asset

- Collateral amount

- Payment amount

- Number of payments

- Payment interval

- Start date

- Maximum missed payments allowed

- Maximum overdue value allowed

- Transaction fee

Both sides must agree to the terms.

Once the loan is completed and broadcast, the chain validates the transaction. If valid, the lent asset moves to the borrower and the collateral becomes locked according to the loan terms.

This is important: the blockchain itself understands the loan. It is not guessing based on arbitrary smart contract bytecode. The loan is a native transaction type with native validation rules.

⏰ Payment Schedules Are Built Into the Loan

Contractless loans support scheduled payments.

The loan has a start time and a payment interval. Payments are calculated from the loan timestamp/start date rules and validated by the node.

A borrower can make payments over time using loan payment transactions.

A key detail is that Contractless does not simply count the number of payment transactions and assume each one is a full payment.

That would be easy to abuse.

For example, imagine a borrower owes five payments of 210 CLTC. If they send five payments of 1 CLTC each, they have not truly made five payments. They have paid only 5 CLTC.

Contractless handles this by tracking the total amount paid against the total amount that should have been paid.

That means partial payments can be useful, but they do not magically satisfy the loan unless they add up correctly.

This allows flexibility without letting borrowers exploit the payment count.

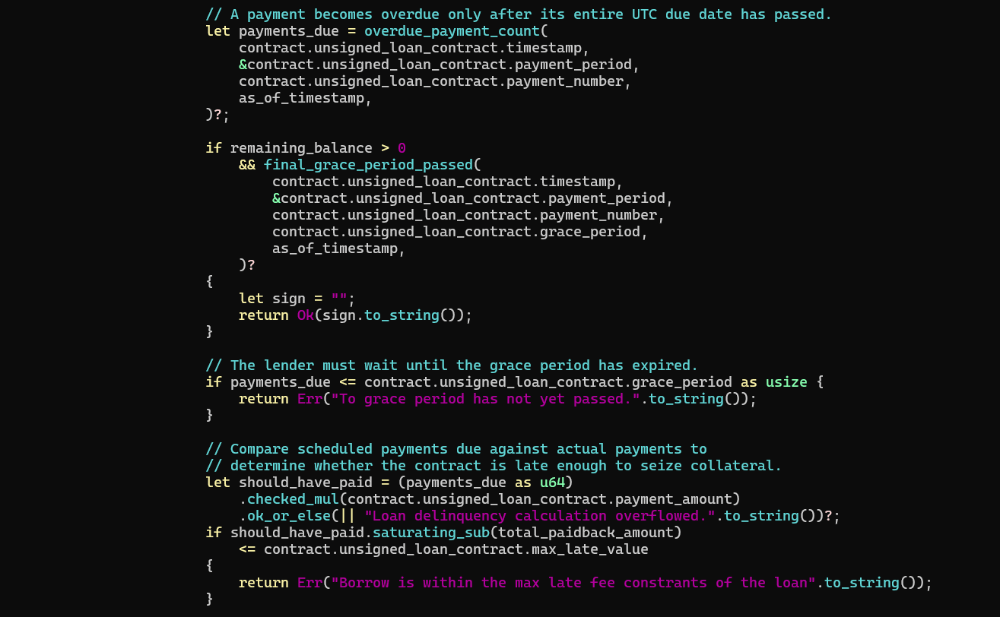

🧮 Collateral Claims Require Clear Conditions

Collateral claiming is one of the most important parts of Contractless loans.

Many lending systems trigger liquidations based on a single collateral ratio. Contractless loans use terms defined in the loan itself.

For most of the loan period, a lender cannot claim collateral just because they feel uncomfortable. The borrower must be behind according to the loan rules.

The important part is that collateral claiming is based on both:

- How many payments are overdue

- How much value is overdue

This matters because one condition alone can be misleading.

If a borrower is technically behind by time but only owes a tiny amount, immediate collateral seizure may be unfair.

If a borrower owes a large amount but is still within the allowed payment/grace window, immediate collateral seizure may also be unfair.

Contractless loans are designed so that both timing and amount matter.

🧾 The Final Payment Rule

There is one important exception.

At the end of the full loan term, after the allowed grace period, any remaining unpaid balance can allow collateral claim.

This prevents an edge case where a borrower could leave a tiny amount unpaid forever and avoid collateral claim because they were not overdue by enough value.

For example:

A borrower owes 100 per day.

The allowed overdue value is 100.

The borrower pays everything except 99.

Without a final maturity rule, the lender might be stuck unable to claim collateral even though the loan was never fully repaid.

Contractless avoids that.

Once the loan term and grace are over, unpaid remaining balance matters. The loan must actually be paid off.

🪙 Loan Payments Must Include Miner Tips

Loan payments also include miner incentives.

A loan payment has a base transaction fee paid in the base currency, and it muse also include an asset-denominated tip paid in the loan asset.

This matters because miners are the ones selecting and including transactions in blocks. When a payment includes an additional tip, that can make the transaction more attractive to miners who then earn in currencies other than just the base currency of the chain.

The key detail is that the tip does not count as repayment to the lender.

The lender receives the payment amount.

The miner receives the tip.

The borrower must have enough for both.

This keeps accounting clear.

🛡️ Why This Is More Decentralized

Contractless loans are decentralized because the loan logic is handled by the blockchain protocol itself.

There is no platform custody.

There is no lending pool operator.

There is no smart contract admin key.

There is no protocol treasury deciding loan terms.

There is no centralized lender managing user funds.

The two parties define the loan.

The blockchain validates it.

The chain enforces the results.

That is the core idea behind contractless loans.

They are not “decentralized” because a website says they are. They are decentralized because the lending mechanism is native to the chain and does not require a third-party platform to hold, pool, or manage the assets.

🏗️ Why Native Loan Transactions Matter

Most blockchains treat loans as an application-layer problem.

That usually means someone has to build a lending app, deploy smart contracts, manage liquidity, create interfaces, handle liquidations, and hope the system behaves during stress.

Contractless treats loans as a base blockchain capability.

This gives several advantages:

- Nodes validate loans consistently.

- Wallets can understand loans directly.

- Loan history can be displayed natively.

- Borrowers and lenders can see terms without trusting a third-party website.

- Payments and collateral claims are standard transaction types.

- Loan accounting can be reconciled directly in the wallet.

This is especially important for user experience.

A wallet should not need to treat loans as mysterious smart contract interactions. It should be able to show:

- Active loans

- Whether the user is lender or borrower

- Payment history

- Remaining balance

- Next payment due

- Collateral status

- Claim eligibility

That is the direction Contractless takes.

🧠 Contractless Loans Aren't Matchmakers

One important distinction: Contractless loans are not automatically a lending marketplace.

The blockchain provides the loan transaction types and validation rules. It does not force a specific marketplace, order book, or matching system.

That is intentional.

Different apps can build different matchmaking experiences on top of Contractless:

- Private lender-borrower matching

- Public loan offers

- Business credit markets

- Collateralized asset lending

- Stablecoin lending

- NFT/RWA-backed lending

- Peer-to-peer credit groups

But the loan itself remains native to the chain.

This separates the protocol from the marketplace.

A marketplace can disappear, but the loan transaction still exists on chain.

🏦 Real-World Style Lending Without Banks

Contractless loans are closer to traditional loans than most DeFi lending models.

In traditional lending, a borrower and lender agree to terms:

- How much is borrowed

- What collateral is provided

- When payments begin

- How often payments are due

- What counts as default

- What happens if the borrower fails to pay

Contractless brings that structure on chain.

That makes it possible to model loans in a way that feels more familiar. A borrower does not necessarily owe the first payment the instant the loan is created. Payments can begin according to the loan’s start date and interval.

This matters because real loans usually have payment schedules.

If someone takes a loan today, they are not normally expected to make the first payment five seconds later. The payment schedule is part of the agreement.

Contractless loans were designed with that kind of real-world expectation in mind.

🌉 Why This Matters for Stablecoins and RWAs

Contractless loans become even more interesting when paired with tokens, stablecoins, NFTs, and RWAs.

Imagine a borrower receives a stablecoin loan and uses CLC or another asset as collateral.

Or imagine a lender accepts an RWA-backed NFT as collateral.

Or a business uses Contractless data storage and loan transactions together to build a decentralized credit application where users own their own data and sign their own loan terms.

The key point is that the loan mechanism is not limited to one platform’s imagination.

Because Contractless supports multiple native transaction types, loans can interact with a broader ecosystem of assets.

That creates room for lending models that are difficult to build cleanly on chains where everything depends on custom smart contracts.

🚫 What Contractless Loans Do Not Claim

It is important to be honest: Contractless loans do not remove all lending risk.

They do not magically make every borrower trustworthy.

They do not guarantee collateral will keep market value.

They do not force people to agree to good terms.

They do not replace due diligence.

They do not eliminate volatility.

What they do is remove unnecessary platform risk from the loan structure.

The lender and borrower still need to make good decisions.

But they are not forced to route that agreement through a liquidity pool, a centralized lender, or a smart contract platform with extra layers of control.

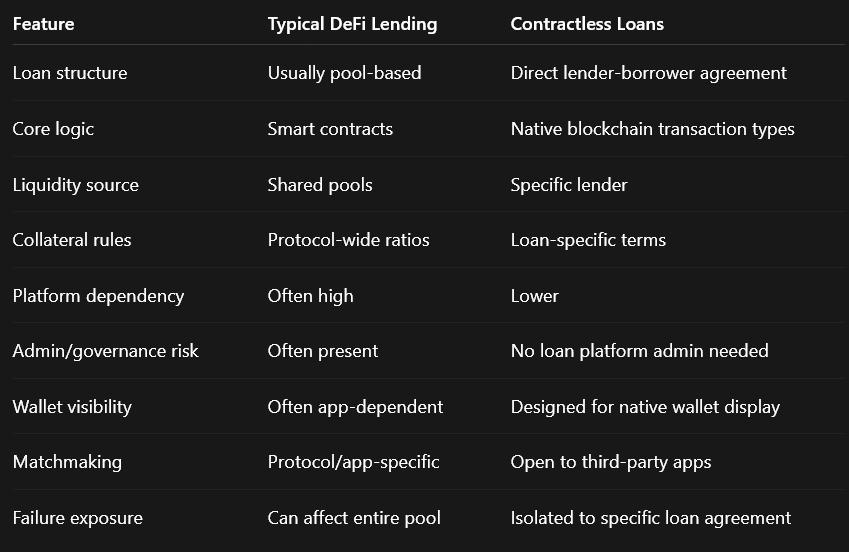

🔍 Contractless Loans vs Typical DeFi Loans

🧭 Why Contractless Loans Are Different

The goal is not to recreate DeFi lending with different branding.

The goal is to build decentralized loans from the ground up.

Contractless loans are different because they are:

- Native to the blockchain

- Direct between lender and borrower

- Not dependent on liquidity pools

- Not dependent on smart contract platforms

- Validated by nodes

- Visible to wallets

- Structured around real loan terms

- Flexible enough for tokens, stablecoins, NFTs, and RWAs

This gives Contractless a lending model that is more transparent, more direct, and easier to reason about.

🚀 The Bigger Picture

The phrase “decentralized loans” should mean more than depositing into a platform and hoping the protocol survives the next crash.

It should mean that two parties can form a loan agreement directly, with clear terms, clear collateral, clear payments, and blockchain-level enforcement.

That is what Contractless loans are trying to make possible.

The Contractless blockchain was built around the idea that money, assets, loans, swaps, NFTs, marketing records, and app data should not all require external smart contracts just to exist.

Some things should be native.

Loans are one of them.

Contractless loans are not just another DeFi product. They are a different way of thinking about decentralized lending itself.

💬 Interested in Contractless Loans?

Contractless is currently in testnet development.

If you are interested in decentralized loans, native blockchain lending, or running a Contractless testnet node, check out our source code, docs and whitepaper which can all be found at:

https://contractless.dev/contractless/Contractless