DeFi is (kind of) growing up

Can you feel it in the air?

Maybe it’s the market rallying, or it’s the old guard of crypto finally being flushed out, or the regulatory and institutional blessings seemingly on the horizon. We might not be able to pinpoint what the catalyst is exactly, but there’s no doubt that the times are changing. The timeline is uncertain—it’ll probably somehow still catch us off guard—but the path to bull market and the next cycle is more likely than not, slowly making its way to us.

And in this pre-ordained path to riches or ruin, how will the applications we interact with change?

The most widely used application for crypto over the last few years has been DeFi, which makes sense. Blockchains have clear potential for enabling stores of value and mediums of exchange, and at the same time, they’re fantastic at enabling speculation and trading (which is what most users coming to crypto use it for). But as crypto slowly makes its way back into the mainstream, and as we attempt to build lasting relevance, DeFi may not look exactly like it did in the past.

We’re already seeing more of a synthesis between applications and the underlying infrastructure, which will may lead to both more application-focused development and value accrual wars. Unsurprisingly, big applications and protocols are also vying to get bigger, which is good for users, onboarding, and our overall experience; but the playing field has to be level enough for even the smallest teams to readily compete with them. And in the longer term, I see the industry trending towards becoming both more mature and blue-chip on one side and more risk-taking/niche on the other, which is an important balance to strike if we want crypto to become big but have a unique advantage over TradFi.

DeFi and infrastructure overlap

One of the big themes of this past year has been the rejuvenation of the appchain thesis, catalyzed primarily by a few factors:

- The growth and success of layer 2s, evidenced by the significant surge in their usage, TVL, fees etc.

- The subsequent proliferation of layer 2 SDKs (OP Stack, Arbitrum Orbit, Polygon CDK, ZK Stack) and RaaS providers (too many for me to count)

- The Lindy-ness and continued development of the Cosmos and Solana ecosystems, especially through the bear market

In short, it’s now both technically trivial and potentially lucrative for projects to become appchains and/or rollups. Other pieces of infrastructure, like oracles, have already successfully taken the appchain approach, but now DeFi projects are increasingly adopting this framework. On the OP Stack, we have derivatives through Lyra, Aevo, and IntentX; on Polygon CDK we’ll have perps with IDEX and RWAs (sorry, neofinance) with Canto; and many more are popping up within and beyond the EVM ecosystem.

This shift isn’t just a technical evolution; if anything, it’s a competitive and strategic one. DeFi providers, now more than ever, are competing with entire networks and are looking to capture more value in the infrastructure stack. And while this push towards vertical integration can be beneficial for smaller, newer teams, the shift will be still led by the leaders and incumbents. Those are the protocols with strong moats, treasuries, and communities with enough demand to create a gravitational force to their network. The result? Big applications will get probably bigger, absorbing more of the value and infrastructure surrounding them, retaining users within their ever-growing ecosystems. And although it sometimes goes unspoken, absorbing more revenue is absolutely a deciding factor in going the appchain route. Dymension, a RaaS provider, clearly declares that “crypto apps are in dire need of ease of use and economic sustainability” and that the rollup business model is a proven way to get cash flow. I’m personally not convinced that this is a strong rationale—that a business must own the vertical supply chain in order to cover its costs. Maybe it’s just not a good enough business! But this is only one small example and there are other rationales that do appeal to me—let’s look at a few cases where this topic was discussed more in-depth:

And although it sometimes goes unspoken, absorbing more revenue is absolutely a deciding factor in going the appchain route. Dymension, a RaaS provider, clearly declares that “crypto apps are in dire need of ease of use and economic sustainability” and that the rollup business model is a proven way to get cash flow. I’m personally not convinced that this is a strong rationale—that a business must own the vertical supply chain in order to cover its costs. Maybe it’s just not a good enough business! But this is only one small example and there are other rationales that do appeal to me—let’s look at a few cases where this topic was discussed more in-depth:

Maker

The conversation around this topic was most heavily ignited last year when MakerDAO’s Rune controversially claimed that Solana would be the best choice for their ‘NewChain’. The justification rested upon Solana’s efficiency (fair enough) and apparently, its ability to hard-fork (huh?). The crypto community immediately descended upon twitter and the forum to either hurl indecencies and question Rune’s intelligence, or revel in excitement and pitch their particular solution. facts or salty? you decide.

facts or salty? you decide.

facts or salty? you decide.

While a lot of the discourse was dominated by opinionated bagholders (salty ETH ones and euphoric SOL ones to be specific), the community did raise important questions about Maker’s potential centralization and value capture:

- Should Eth devs let Maker double-dip by tapping both Sol and Eth developer communities as they claim they can?

- Is this an attempt to instate another key stablecoin and become financially ‘too-big-to-fail’ to that network as well?

- Is this undue focus on hard-forking too much of a centralizing force?

Other good counterpoints were also made—namely, who gives a shit about Ethereum-alignment when this is a product that’s envisioned for the entire world, untethered to a particular ideology (except in context of its primary tokenholders)? Is it destructive to restrain a protocol just because it was initially built on your network? This whole fiasco reminds me a bit of when dydx decided to move to Cosmos, though I think that was still a bit better received. And while the circumstances and motivations surrounding the decision are still debated—to the team’s credit—they’ve actually committed fully to the Cosmos tech stack and are working with teams in the ecosystem like Skip to build mechanisms all the way down to the block level (not currently viable in Ethereum). If Maker were able to provide a more thorough explanation, and reference what they could uniquely leverage elsewhere, the response may have been (slightly) better.

This whole fiasco reminds me a bit of when dydx decided to move to Cosmos, though I think that was still a bit better received. And while the circumstances and motivations surrounding the decision are still debated—to the team’s credit—they’ve actually committed fully to the Cosmos tech stack and are working with teams in the ecosystem like Skip to build mechanisms all the way down to the block level (not currently viable in Ethereum). If Maker were able to provide a more thorough explanation, and reference what they could uniquely leverage elsewhere, the response may have been (slightly) better.

Maker has been an undeniable pillar of the DeFi industry from the very beginning. It, of all protocols, has the ability to shift the entire focus of chains and communities to its needs, and it seems like they believe it’s the right next step for the market. Creating its own chain could very well be critical to its Endgame strategy, but it’s definitely left us thinking about the motivations and the tradeoffs therein.

L2s (Frax and others)

I listed quite a few appchain L2s earlier, but I think Frax’s upcoming one will exemplify the value-capture debate and signal a trend for the rest of the industry. Frax is a top contender in the staking and stablecoin market, and it has other DeFi components as well (more on this later). In Mid 2023, founder Sam Kazemian announced Fraxchain, a hybrid optimistic/ZK L2 (TBD on which stack they’re building on). Sam makes interesting arguments for building an appchain, like creating a monetary premium for their LST product, sfrxETH, and experimenting with yield in ways that reward the users for inherently participating onchain.

It seems pretty interesting and there’s a lot of potential from how he’s describing it. And from a value-capture perspective, this is killer: this approach allows them to build out an entire ecosystem with their gas token, a stablecoin, an LST, and more; this will effectively become a one-stop shop for the majority of a user’s DeFi needs, and all of that value flows within the Frax system. Of course, we also can’t discount the competition-related reasons for starting an L2. Building an appchain gives them a unique angle compared to the dominant players in liquid staking (Lido) and stables (USDT, USDC, etc.), so it’s not all user or tech-based. I think Base, OKX’s X1, and Kraken’s upcoming L2 are great parallels to Frax that also highlight this trend clearly, despite not playing in the application layer—yet. They’re general-purpose, not appchains, but their parent companies all compete in the retail application space through their centralized exchanges; the motivation to create L2s for them is obviously to expand their offering and capture more revenue through the symbiosis of their onchain + offchain products. And while they may remain in the infra space right now, I can bet money that they’ll start building DEXs and other applications on their L2s; the opportunity for value capture and bundling is too good for them to pass up (as an aside, this is exactly why Scroll’s vision is to remain purely infra; we want to let builders build on us without competing with them). The difficult equilibrium here is that it probably is more efficient and user-friendly if the apps and infra are all bundled up and delivered by one team; but the downside is obviously the risk of centralization and not really using the ‘DeFi money legos’ we’ve built.

I think Base, OKX’s X1, and Kraken’s upcoming L2 are great parallels to Frax that also highlight this trend clearly, despite not playing in the application layer—yet. They’re general-purpose, not appchains, but their parent companies all compete in the retail application space through their centralized exchanges; the motivation to create L2s for them is obviously to expand their offering and capture more revenue through the symbiosis of their onchain + offchain products. And while they may remain in the infra space right now, I can bet money that they’ll start building DEXs and other applications on their L2s; the opportunity for value capture and bundling is too good for them to pass up (as an aside, this is exactly why Scroll’s vision is to remain purely infra; we want to let builders build on us without competing with them). The difficult equilibrium here is that it probably is more efficient and user-friendly if the apps and infra are all bundled up and delivered by one team; but the downside is obviously the risk of centralization and not really using the ‘DeFi money legos’ we’ve built.

Thoughts

So it’s clear that DeFi, the largest application segment of the market, is expanding into infrastructure and the appchain / rollup space as it matures. But why does it matter? Why shouldn’t they do so? Appchains do in fact solve relevant needs in DeFi (e.g., low latency, high-throughput limit order books that need increased scalability). But they also come with heavy tradeoffs for users, like fragmentation of liquidity and poor UX due to excessive bridging. Until we solve those issues or reach a point of near-complete network abstraction for the user, this will make switching between and using applications significantly more difficult than it already is.

Even so, part of me, especially as a user, is quite excited about this potential of application-driven infrastructure development and usage, since it’s been so backwards for so long. If these applications really are driving usage, let them proliferate and lead the way! That’s the permissionless nature of the market at work. These apps have just as much right to ‘own’ the stack as infra providers do.

Yet the other part of me, especially as a cynic, worries that this is but another attempt at opportunistic value capture and fragmentation that’ll primarily benefit incumbents. Spout as much open-source protocol friendliness and collaboration you’d like; the bottom-line is that they’re all still competitors, and still roughly follow the competitive market dynamics we’re used to outside of crypto. If there’s an opportunity to ensnare more value within applications, even if it’s at the expense of the users’ experience, some teams will go for it. It comes back to the debate between the fat protocol and fat app thesis; who really ‘owns’ the users and their onchain interactions? The implications of this question are the critical drivers for L2s releasing SDKs in the first place. They’ve gotten ahead of the problem a little bit since anyone with a stack will capture revenue from its appchains, but the same push and pull will continue to persist; protocols big enough to justify appchains are incentivized to and usually able to build out their own infra and capture revenue from there. It’s still too early to tell how the DeFi and infra overlap will play out, but there’s definitely going to be a reckoning about value accrual and rent-seeking.

It comes back to the debate between the fat protocol and fat app thesis; who really ‘owns’ the users and their onchain interactions? The implications of this question are the critical drivers for L2s releasing SDKs in the first place. They’ve gotten ahead of the problem a little bit since anyone with a stack will capture revenue from its appchains, but the same push and pull will continue to persist; protocols big enough to justify appchains are incentivized to and usually able to build out their own infra and capture revenue from there. It’s still too early to tell how the DeFi and infra overlap will play out, but there’s definitely going to be a reckoning about value accrual and rent-seeking.

Expanding protocol scope and influence

Similar to the app + infra consolidation, many DeFi protocols are also expanding their services, offering full product suites and introducing features like stablecoins that expand the scope of their influence. In a way, many of them seem more analogous to full on businesses and mini-empires as opposed to single-focus applications now.

Expanding beyond DeFi

Going forward, some projects will opt to expand their scope and breadth, aiming to create pseudo-conglomerates that include, but don’t begin or end with DeFi. Probably the most pivotal moment spurring this trend has already happened—Aave’s recent acquisition of the Family wallet team, and subsequent rebrand into Avara. This signals to me the beginning of real DeFi ‘companies’, though I doubt they will or should brand themselves as such. There’s a formidable group under this Avara umbrella: Aave, the king of lending; Lens, a leading social protocol; GHO, Aave’s stablecoin; Sonar, a metaverse mobile app; and now Family. The vision here is clear. You own the user’s end to end experience through the wallet, onboard and engage them on the social side, and power their key DeFi needs, all in an ostensibly unified experience.

We’re definitely going to see more of this sort of expansion across the industry. Polygon is a great example of another (not specifically DeFi) company that may very well trod down this path. They’re already well-acquainted with leveraging M&A to build out their teams, and although much of their focus is on infra, it would be strategic and brand-aligned for them to expand deeper into the application and DeFi space. If the goal is to truly own the funnel from end to end, what better way to do so than to own the infra, the tools to interact with the chain, and the applications on the chain itself? As with vertical integration, this type of expansion is primarily a strategy for the bigger players. However, we might start to see more smaller protocols group together into joint ventures as collectives. The question, as we shift into this space of mergers and collectives, is how to maintain effective decentralization (assuming that’s still the goal). How will the DAO structure work across a group of various teams, each with different user bases, tokens, and levels of influence? How do we prevent rent-seeking, centralization, and all the other toxic aspects of web2 from creeping into these increasingly larger protocols? The question will become more and more critical as our favorite, well-known applications evolve and broaden their reach.

The question, as we shift into this space of mergers and collectives, is how to maintain effective decentralization (assuming that’s still the goal). How will the DAO structure work across a group of various teams, each with different user bases, tokens, and levels of influence? How do we prevent rent-seeking, centralization, and all the other toxic aspects of web2 from creeping into these increasingly larger protocols? The question will become more and more critical as our favorite, well-known applications evolve and broaden their reach.

Expanding within DeFi

Other projects are expanding their scope by building out DeFi ‘empires’: they’re what I would describe as sets of interconnected DeFi protocols meant to power their flywheels, give users unified experiences, and bring more value to the entire collective and its underlying components. Plenty of apps incorporate multiple DeFi features, but the distinction here is that there’s an attempt to compound the benefits of these features upon each other and power the internal DeFi engine with its respective token. There’s a few exciting teams building out these types of products, and it’s worth quickly highlighting a few and explaining what they do:

- Frax: Started as a collateral + algorithmic stablecoin, now expanded into other stable assets, an LST, an AMM, RWAs, a lending market, and now becoming an L2 as well.

- Redacted Cartel: Started initially as an OHM Fork. Now evolved into group with Hidden hand, a governance token bribe marketplace (think Convex); Pirex / pxETH, LST products; and Dinero, a stablecoin.

- Oath: Built by the Bytemasons team, consists of Granary, lending market; Ethos Reserve, CDP stablecoin; Digit, maturity-based yield primitive; and Reaper Farm, yield optimizer for the above protocols. All linked through OATH Token; uses chapter model with unique protocols on different chains (e.g., the newly launched AureliusFi on Mantle).

All of these projects have different approaches, but if we look for areas of overlap, it’s pretty illuminating about the next stage of DeFi and what mature protocols are looking to prioritize going forward in this cycle. There’s a few core primitives shared amongst them all:

- Establishing a foundational, proprietary medium of exchange (stablecoin, LST, or both)

- Frax has FRAX, FPI, frxETH, and sfrxETH; Redacted has pxETH and Dinero; and Oath has ERN (Ethos Reserve) + more assets within individual chapters.

- System designed to profit from liquidity flows (irrespective of the liquidity recipient)

- Frax has an in-house AMM, lending protocol, bridging, and gauges, but more importantly, is building an L2 to truly capitalize on liquidity and tx flows; Redacted uses Hidden Hand to profit on liquidity wars across different protocols, regardless of the winner; Oath’s interconnected Reaper Farm allows the protocol to maximize and benefit from much of the liquidity interacting with its system across each new chapter.

- Mechanism to accrue protocol-owned-liquidity

- Frax’s AMO stablecoin and all other aspects of the protocol are designed to provide fees and protocol owned liquidity (they even have a nice little balance sheet here!); Redacted’s design originated from Olympus—the progenitor of POL—and since then it’s migrated to a more sustainable token model, benefitting from Hidden Hand + Pirex fees, and Dinero’s liquidity will compound from all of these pieces; Oath’s Reaper Farm, again, orchestrates and captures liquidity, and the DAO is moving towards an options-token model (à la Velocimeter and Tapioca) that is specifically designed around POL.

What do these similarities tell us about the goals and evolution of DeFi?

First—the fundamental truth that stables, and by extension, mediums of exchange, are the most obvious product-market fit of crypto and the most powerful tool in the industry. They’re necessary if we want everyone in the world to transact with each other onchain; we can’t onboard users without assets with deep liquidity and/or safety from volatility. Like real currencies, they are dominant stable/liquid-staked assets, large enough to influence the consensus of the underlying chains in a worst-case scenario. It’s a no-brainer that a large enough DeFi protocol will want to own this crucial primitive, and that the three listed here have stables, LSTs, or both. After all, Maker built their billion dollar business on that alone. It’s not just these guys above, too—other market leaders like Curve and Aave have been taking a stab at the stablecoin business as well. Overall, I’d argue this is actually positive for the industry. We’re all a bit wary after UST’s collapse but we also don’t want to solely rely on centralized solutions, so this is avenue for experimentation and an opportunity to actually build sustainable, decentralized mediums of exchange. And second—liquidity is still king, but we need to capture and benefit from it in newer, more efficient ways. We’re seeing a marked departure from the naive implementations of liquidity incentivization and revenue generation, with some teams even declaring that liquidity mining is dead. Instead, these teams are capturing fees through the flow of liquidity across other protocols and within their own protocols through: owning base layer infra, capitalizing on competitive liquidity elsewhere, or expanding branches of their protocol into a unified layer as opposed to various fragmented instantiations. And they’re building tools to generate and keep liquidity in-house instead of fighting for it, building up the ability to sustain their tokens and communities. It’s clear that apps are bountiful but money is not. If you want to expand, it may not be enough to deploy everywhere and blindly reward users—you need to have tight control over how the value comes to your application, and how to maintain it in a sustainable way.

And second—liquidity is still king, but we need to capture and benefit from it in newer, more efficient ways. We’re seeing a marked departure from the naive implementations of liquidity incentivization and revenue generation, with some teams even declaring that liquidity mining is dead. Instead, these teams are capturing fees through the flow of liquidity across other protocols and within their own protocols through: owning base layer infra, capitalizing on competitive liquidity elsewhere, or expanding branches of their protocol into a unified layer as opposed to various fragmented instantiations. And they’re building tools to generate and keep liquidity in-house instead of fighting for it, building up the ability to sustain their tokens and communities. It’s clear that apps are bountiful but money is not. If you want to expand, it may not be enough to deploy everywhere and blindly reward users—you need to have tight control over how the value comes to your application, and how to maintain it in a sustainable way. Interestingly, most of these full DeFi product suites are currently seen as less than a sum of their parts, at least if indicated by their token prices. That’s likely due to a few factors: it’s narratively simpler to pump a singular application’s token, and usually most of these are traded on the value of their primary product; the product suite has to compete effectively across most, if not all of its branches and prevent value leakage; this DeFi product suite concept is generally still pretty new; and most tokens have still been on a recovery path since 2022. In theory, these product suites can be pretty attractive to users. If you’re already using one product or interested in one—whether it’s a liquid staking derivative or a lending platform—you can gain significant financial upside by participating further in that ecosystem and fulfilling the rest of your DeFi needs there. This all does come back to the same concern over centralization and potential rent-seeking we discussed in the first section; but quite frankly, the issues faced by current DeFi protocols that are looking to be solved here are just as bad, if not worse. It is important for the industry to attempt to build applications that can actually last in the long-term and build a symbiotic relationship with users.

Interestingly, most of these full DeFi product suites are currently seen as less than a sum of their parts, at least if indicated by their token prices. That’s likely due to a few factors: it’s narratively simpler to pump a singular application’s token, and usually most of these are traded on the value of their primary product; the product suite has to compete effectively across most, if not all of its branches and prevent value leakage; this DeFi product suite concept is generally still pretty new; and most tokens have still been on a recovery path since 2022. In theory, these product suites can be pretty attractive to users. If you’re already using one product or interested in one—whether it’s a liquid staking derivative or a lending platform—you can gain significant financial upside by participating further in that ecosystem and fulfilling the rest of your DeFi needs there. This all does come back to the same concern over centralization and potential rent-seeking we discussed in the first section; but quite frankly, the issues faced by current DeFi protocols that are looking to be solved here are just as bad, if not worse. It is important for the industry to attempt to build applications that can actually last in the long-term and build a symbiotic relationship with users.

The barbell effect in DeFi

The final theme that will start to play out over the next cycle—though we won’t really see the full effects for a couple of years—is the barbell effect taking place in DeFi. Multitudes of applications and their users will get pushed out to the edges, either to the ever-growing market leaders like the ones discussed above, or further out towards the niche, long-tail, and end-of-the-risk-curve side of things.

Blue chips & boomers side of barbell

Some consider it apocalyptic and antithetical to the cypherpunk ethos, while others are praying for the sake of their bags that it saves them.

Shill it, FUD it, the normies and tradfi will arrive all the same. The boomer-ification of DeFi & crypto at large is well along on its way, especially once the market finally heats back up. Now that we’re over Starbucks NFTs and paying sports betting platforms to run validators, it’s time for the big boys at the banks to start tokenizing assets and for institutions to start getting involved onchain again. This is where the collectives, DeFi empires, stablecoin issuers, top appchains, etc. can be at a serious advantage, as they’re the most likely to capture the newly onboarded users and drive value from them. There will be compounding effects from both institutional and retail users on this more ‘blue-chip’ side of the market. We might even start to see more focus on boomer web2 business fundamentals: revenue, costs, profit (crazy, I know).

The boomer-ification of DeFi & crypto at large is well along on its way, especially once the market finally heats back up. Now that we’re over Starbucks NFTs and paying sports betting platforms to run validators, it’s time for the big boys at the banks to start tokenizing assets and for institutions to start getting involved onchain again. This is where the collectives, DeFi empires, stablecoin issuers, top appchains, etc. can be at a serious advantage, as they’re the most likely to capture the newly onboarded users and drive value from them. There will be compounding effects from both institutional and retail users on this more ‘blue-chip’ side of the market. We might even start to see more focus on boomer web2 business fundamentals: revenue, costs, profit (crazy, I know). But there’s still a serious barrier to this side of DeFi. When thinking about appealing to the ‘next billion users’ or the institutions, it’s not merely a UX issue; it’s a question of opportunity cost and risk/reward. As we enter any DeFi application, we open ourselves up to an innumerable set of risks: including credit and counterparty risk, smart contract risk, liquidity risk, and naturally, systemic risk within or across blockchain networks. Crypto natives are used to both the excitement of eye-watering yields and the terror of helplessly watching their funds get drained. We’ve acclimated to accepting the tradeoffs therein because we’re deeply embedded in an ecosystem for financial and/or ideological reasons (with maybe a touch of collective stockholm syndrome). But maybe another 5-10% of the developed-world population (and a larger percentage in the developing world) will be willing to dive into the world of DeFi and speculation. But everyone else, if they’re interacting with anything onchain, will be primarily interested in some basic yield and maybe some swapping / lending to a smaller degree—and there’s still an absurd amount of risk in doing any of that, to a normal person.

But there’s still a serious barrier to this side of DeFi. When thinking about appealing to the ‘next billion users’ or the institutions, it’s not merely a UX issue; it’s a question of opportunity cost and risk/reward. As we enter any DeFi application, we open ourselves up to an innumerable set of risks: including credit and counterparty risk, smart contract risk, liquidity risk, and naturally, systemic risk within or across blockchain networks. Crypto natives are used to both the excitement of eye-watering yields and the terror of helplessly watching their funds get drained. We’ve acclimated to accepting the tradeoffs therein because we’re deeply embedded in an ecosystem for financial and/or ideological reasons (with maybe a touch of collective stockholm syndrome). But maybe another 5-10% of the developed-world population (and a larger percentage in the developing world) will be willing to dive into the world of DeFi and speculation. But everyone else, if they’re interacting with anything onchain, will be primarily interested in some basic yield and maybe some swapping / lending to a smaller degree—and there’s still an absurd amount of risk in doing any of that, to a normal person.

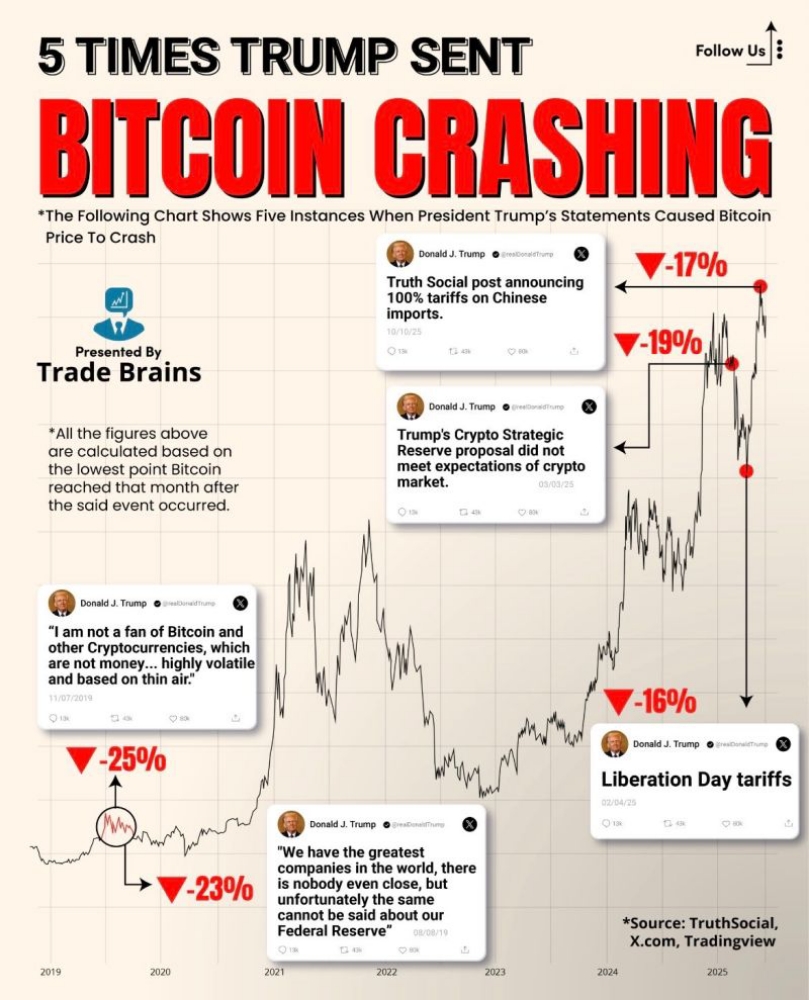

Ask yourself this: is a 20%+ APR in a DEX pool worth it for the non-zero tail-risk that it gets exploited (i.e., 1-5% chance you lose 100%)? Maybe not, but what if the APR is 100%+? That’s not uncommon, after all. Sure, but how long will it last? What incentives are in place to drive that, and keep that sustainable? Will it rug? Let me stop you right there. There’s endless questions and concerns that come up when you think about the risk associated from the perspective of an outsider. Smart contract risk alone is a non-starter for significant chunk of the population because of the implications it has on the expected return. Even OGs like Curve and Kyber, building in the most heavily researched and developed part of the DeFi space, can be subject to protocol-threatening hacks.

There’s a lot of suggestions out there to mitigate against this, but not a ton of obvious solutions. Some suggest raising bounties, but that probably won’t deter many hackers and can lock up even more capital (especially if proposed bounties scale with TVL). Others suggest rethinking and expanding the scope of the EVM (and Solidity / Vyper) or moving away it entirely, though many of those proposals come from teams in other ecosystems with their own motivations. A newer thought I’ve heard is that we start to take more pieces, like certain / all core smart contracts off-chain to avoid state-related exploits and post ZK proofs on chain; this is an exciting new area, but it’s still too early to tell. I’m more than confident that over time we’ll have a clearer picture of trustworthy, battle-hardened protocols, beyond simply Uniswap, Aave. etc. But ideally we want to have many more projects compete in the space, and the path forward there isn’t so clear.

Long tail / degen side of barbell

Up until now, I’ve painted a picture of huge centralizing forces and incumbents, but a big caveat here is that this is a very long term view. The large, proverbial middle of the space will continue to exist for a while because of the permissionless nature of crypto. There’s always an opportunity to make a buck when the cost of spinning up something new is so low and the amount of speculation is so high. That being said, my points in the prior section come into play here—the existing incentive and liquidity models may not be popular forever. If these models wane significantly, we could see a sharp decline – potentially wiping out an easy 30-40% of the DeFi market that's driven largely by the allure of these incentives.

But if we go towards the other side of the barbell, where the niche, degen, and long-tail reside, we’ll find quite a lot of activity continuing to happen there. This is the breeding ground for innovation – where more and more derivatives, complex DeFi solutions, and experimental ideas emerge. Many of these applications will fail, but some of these innovations will inevitably rise to prominence, becoming integral to the broader, more successful spectrum of crypto. This end of the barbell, so to speak, is where crypto has thrived up to this point, and it's set to continue.

We’re going to continue to see the degeners get more degen, the risk-taking get more risky, and the memes to get more memetic. The memecoin side of crypto is especially self-referential and runs through cycles at an accelerated pace. It’s untold where exactly it’ll go; it might burn bright and implode at the end of this cycle or it could persist somehow, as memes do. And things will get more cynical. If the Blast launch has taught us anything, people will eke out any value they can find if there’s an opportunity to get it and a narrative to fuel it.

As I’ve said, this barbell effect is going to take some time to come to fruition, if it does happen at all as i’ve described. But if so, it could be good for crypto, by bifurcating the types of users and serving their separate needs. The squeezing of the middle may also flush out a lot of the zombie protocols that have simply been chugging along, and make for a more focused, less bloated industry.

Parting thoughts

DeFi, as with most of crypto, has to this point been a big experiment. We’re tinkering with lending, trading, and yield mechanisms in trustless, decentralized environments, and leveraging incentives in ways that have never been done before. But truthfully, there’s also been a lot of copying and effortless forking, incentive misalignment, and endless yield re-hypothecation; this comes with the permissionless territory. This next cycle, however, promises some new changes. We’re seeing more of a synthesis between applications and infrastructure, where ideally this leads to application-focused development instead of value accrual wars. Big applications and protocols are getting bigger, which is good for users, onboarding, and our overall experience; but the playing field has to be level enough for even the smallest teams to readily compete with them.

As we start to see larger, more competitive, infrastructure-owning DeFi applications, we should be excited for the possibility for actually sustainable and competitive products. But we need to be even more careful that as applications and protocols grow, we make sure to align the naturally centralizing and competitive market incentives towards the crypto ethos. Otherwise, we’re just building banks and ponzis with extra steps.

There’s a certain sense of bittersweet longing that I’m seeing across crypto—a sort of sense that the wild west days in DeFi are coming to a close, particularly after the next bull run. I think it’s a bit premature and short-sighted; yes, there may not be as many absurd valuations, 10,000x’ers, get-rich quick schemes, and so on. But as the world does make another earnest attempt at adopting some level of crypto, we have an opportunity for unprecedented growth; for it to go from a self-referential playground to a real infinite garden.

SOURCE:

https://mirror.xyz/scrollprotocol.eth/UUj7scmKHHIBtz7JCQ_BPH73J5lY0uSH56owD5eIkyw