How lending works in Defi

How lending works in Defi

When you wish to take out a loan, you generally need to put up collateral. Why? Because your collateral is insurance for your loan. It gives you an incentive to pay back your loan and not run away with the money.

Collateralisation Ratio

In Defi, lending works with overcollateralisation where you as a borrower have to deposit more value than you want to borrow. The exact amount required to be deposited depends on how much you want to borrow and is calculated via a collateralisation ratio:

Collateralisation Ratio = Collateral Amount/Borrow Amount

An example:

- The lending protocol you’re using requires a collateralisation ratio of 200%.This means that for every 100 DAI deposited, you can borrow 50 DAI.

The collateralisation ratio determines the liquidation price, which is the market price of the asset deposited when your collateral will start to be liquidated to pay back your loan. The lower the collateralisation ratio to higher the liquidation price and vice versa. The liquidation price is also determined by the health of the market, the lower the volatility of the market and the token for the underlying collateral, the higher the health of the market, and subsequently the lower the liquidation price. The calculation for this is subject to the lending protocol, but taking AAVE as an example the liquidation price is given by:

Liquidation Price = Market Price of the Collateral/Health Factor

Since your collateral will be liquidated once the value falls below the threshold required by the protocol, you will need to add more collateral or pay back your loan in order to avoid liquidation.

Borrowing more

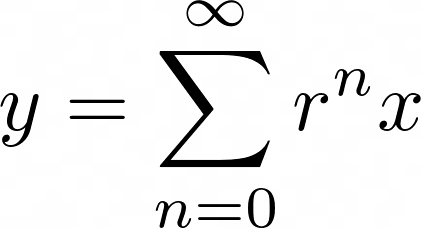

Although you can’t borrow more than your collateral in one go, you can still borrow multiple times your collateral. In order to do so, you simply need to take the borrowed amount from the initial collateral and deposit that again into a lending protocol and repeat the process. Every time you would be borrowing less and less however the total amount summed together would be greater than your initial collateral. The mathematics for this is as follows:

Where y is the final amount obtained, r is the inverse of the collateralisation ratio and x is the collateral amount

Thus this becomes the maximum amount of leverage possible at that collateralisation ratio with that amount of collateral.

What holds Defi Back

One can argue that the financial system we have would be a lot more stable if leverage was lowered and such a scenario would be a byproduct of overcollateralisation. However that is another discussion, and practically speaking, overcollateralisation is one of Defi’s drawbacks. It limits the potential of lending and the utility of financial products.

Be it MakerDAO, Compound, AAVE, or any protocol, all Defi lending companies require borrowers to overcollateralise their assets. And with lending being a significant portion of the Defi TVL (As per Defi Pulse, the current Defi locked-in value stands at $83.21 billion (as of 25/08/2021) with $34.5 billion in lending protocols).

In the real world assuming one’s credit score is sufficient, you can take out a loan greater than your collateral. An example of this is taking out a business loan to start a business. If you have a prior track record of paying back your credit card loans it’s likely you will get a loan larger than the collateral you put up or even receive an unsecured loan.

In order to preserve anonymity in Defi, legal regulation giving debt providers access to their assets if you are unable to pay back your loan is not possible to implement. Hence in order to stop individuals from running away with the money, overcollateralisation is a necessity in the current lending environment.

The future

In order to create much more accessible lending products, collateralisation ratios need to be lowered or collateral entirely removed. One idea is to use a reputation score akin to credit scores in the real world where whitelisted addresses can be lent to based on their history of successfully paying back loans. However, risk can still be possible with users building up a credit score than taking advantage of the system to run away with the funds. In order for that to happen whilst simultaneously securing lender funds, ultimately KYC process may be inevitable.