401K and Roth IRAs what is the difference

Good morning/evening

I heard the news that Donald Trump had signed an executive order about 401Ks being allowed to hold crypto, private equity, real estate and other alternative assets, but as I am not American, and know nothing about this, I also did not know if it was significant or not, so I thought I should take a look, I had also heard of Roth IRAs but did not know the difference so here is what I have found out.

A 401(k) is an employer sponsored retirement plan with high contribution limits and potential employer matches, while a Roth IRA is an individual retirement account that is not tied to employment but has lower contribution limits and strict income eligibility rules. Both offer tax advantages, but 401(k)s provide tax deferred growth on pre tax contributions, whereas Roth IRAs offer tax free withdrawals on after tax contributions and earnings. Ordinary savers will be able to gain access to asset classes previously limited to institutions or wealthy accredited investors, but implementation will take time. So based on this I am not sure it will have much impact at the moment, but may do in the future. I guess it is another step in legitamizing Bitcoin and crypto, but another step towards the corporate TradFi world we are trying to escape from, the double edged sword again!

If an employer offers crypto in their 401(k) menu and employees lose big, lawsuits could follow. Most employers would rather avoid that headache, Adding a small allocation of crypto could diversify retirement portfolios. Crypto doesn’t always move in sync with traditional markets, so it could help balance risk. Millennials and Gen Z, who are driving crypto adoption, also make up the new wave of retirement savers. Forcing them to choose between their 401(k) and crypto could push them away from traditional retirement plans.

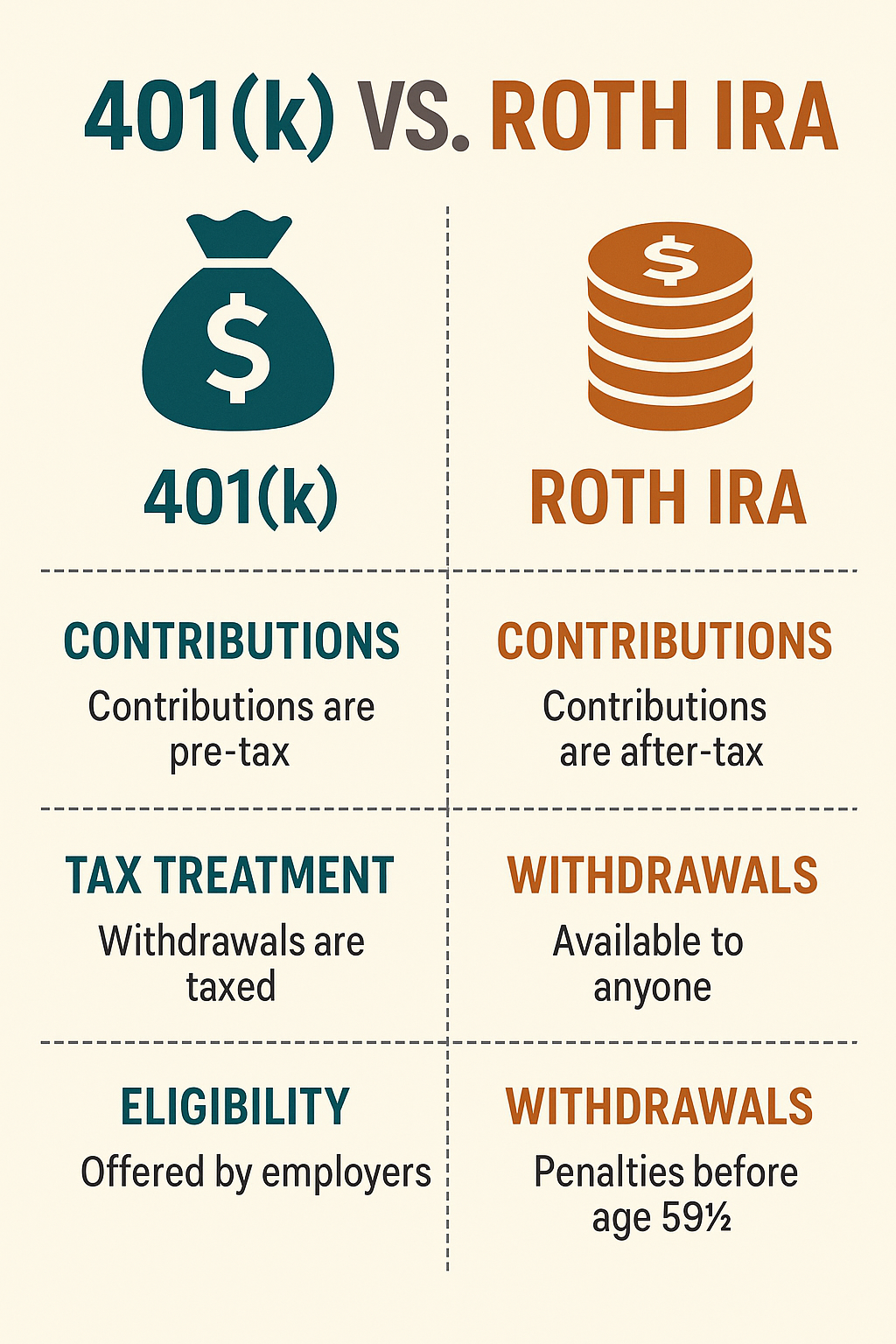

Key Differences

- Sponsorship:401(k): Offered by an employer to its employees.

- Roth IRA: An individual account that you open and contribute to on your own.

- Contributions & Taxes:401(k): Can be pre-tax (traditional) or after-tax (Roth), allowing for immediate tax deductions on pre-tax contributions.

- Roth IRA: Contributions are always made with after-tax money, but qualified withdrawals of earnings are tax-free in retirement.

- Contribution Limits:401(k): Has significantly higher annual contribution limits, allowing for more aggressive retirement savings.

- Roth IRA: Has much lower annual contribution limits compared to a 401(k).

- Employer Match:401(k): Often includes an employer match, where the employer contributes to your account when you do, effectively providing free money for retirement.

- Roth IRA: Not tied to employment, so employer matching is not available.

- Income Eligibility:401(k): Generally no income restrictions on contributing, including Roth 401(k)s.

- Roth IRA: Eligibility to contribute is subject to IRS income limits; high earners may not qualify.

- Withdrawal Flexibility:

- 401(k): Withdrawals before age 59½ are generally subject to taxes and penalties, with some exceptions for hardship withdrawals or if you've left the sponsoring employer.

- Roth IRA: You can withdraw your original contributions at any time for any reason without penalty or taxes, though earnings are subject to taxes and penalties if withdrawn before age 59½ (with some exceptions).

Firtstly I am not sure how this will work out, in regards to your employer matching your contributions but I guess it will be something like an ETF or a crypto fund so it might well not be your preferred crypto, then there will be the volatility aspect which may well put many people off as a 50% drop in a tokens price at the wrong time could reck your retirement plans. But that can also work the other way too and holding certain assets at a certain time could also reward you hugely. Age could also be an importanf tactor, if your young you can leave your pension to work for you for longer, the volatility is less relevant as opposed to smeone like me who is a couple of years away from being able to claim my private pension.

Crypto in 401(k)s could be good in small doses, maybe as a 1–5% allocation because it brings legitimacy, aligns with younger workers, and gives people exposure in a tax-advantaged way. But don’t expect employers to rush into it soon, since volatility and regulation are big hurdles.

When you self-custody Bitcoin, you step outside the financial system entirely. Owning your private keys means you’re in full control, no banks, no custodians, no plan administrators. This sovereignty is powerful and your wealth is portable, censorship-resistant, and available 24/7 across the globe. For many, it’s not just an investment but an ideology, a hedge against inflation, government overreach, or the fragility of traditional finance. With Bitcoin, you don’t just hold an asset you hold freedom.

But with that freedom comes serious responsibility. There are no tax shelters like in a 401(k), no employer match, and certainly no helpline if you forget your seed phrase. Every sell or swap can trigger a taxable event, and the volatility can be brutal, 70% drawdowns are not uncommon. Self-custody demands both technical competence and emotional resilience. Lose your keys, and your Bitcoin is gone forever. It’s a high-risk, high-reward path where the upside is total independence, but the downside is absolute loss.

The fees will also need to be considered, it may well be just as easy to not use a 401k and just buy and self custody your own Bitcoin or crypto. So I am not convinced that this will be a gamechanger yet but you never know. What are your thoughts? Do you think this is good for Bitcoin and crypto?

As always thank you for raeding and please feel free to comment.