What Is Blockchain?

BLOCKCHAIN OVERVIEW

BLOCKCHAIN IS MOST SIMPLY DEFINED AS A DECENTRALIZED, DISTRIBUTED LEDGER TECHNOLOGY THAT RECORDS THE PROVENANCE OF A DIGITAL ASSET. | IMAGE: SHUTTERSTOCK

BLOCKCHAIN IS MOST SIMPLY DEFINED AS A DECENTRALIZED, DISTRIBUTED LEDGER TECHNOLOGY THAT RECORDS THE PROVENANCE OF A DIGITAL ASSET. | IMAGE: SHUTTERSTOCK

What Is Blockchain Technology?

Blockchain, sometimes referred to as distributed ledger technology (DLT), makes the history of any digital asset unalterable and transparent through the use of a decentralized network and cryptographic hashing.

A simple analogy for how blockchain technology operates can be compared to how a Google Docs document works. When you create a Google Doc and share it with a group of people, the document is simply distributed instead of copied or transferred. This creates a decentralized distribution chain that gives everyone access to the base document at the same time. No one is locked out awaiting changes from another party, while all modifications to the document are being recorded in real-time, making changes completely transparent. A significant gap to note however is that unlike Google Docs, original content and data on the blockchain cannot be modified once written, adding to its level of security.

Of course, blockchain is more complicated than a Google Doc, but the analogy is apt because it illustrates critical ideas of the technology.

BLOCKCHAIN MEANING: BLOCKCHAIN EXPLAINED

- A blockchain is a digital ledger or database where encrypted blocks of digital asset data are stored and chained together, forming a chronological single-source-of-truth for the data.

- Digital assets are distributed, not copied or transferred.

- Digital assets are decentralized, allowing for real-time accessibility, transparency and governance amongst more than one party.

- Blockchain ledgers are transparent — any changes made are documented, preserving integrity and trust.

- Blockchain ledgers are public and constructed with inherent security measures, making it a prime technology for almost every sector.

Why Is Blockchain Important?

Blockchain is an especially promising and revolutionary technology because it helps reduce security risks, stamp out fraud and bring transparency in a scalable way.

Popularized by its association with cryptocurrency and NFTs, blockchain technology has since evolved to become a management solution for all types of global industries. Today, you can find blockchain technology providing transparency for the food supply chain, securing healthcare data, innovating gaming and overall changing how we handle data and ownership on a large scale.

WHAT IS BLOCKCHAIN? | VIDEO: SIMPLY EXPLAINED

How Does Blockchain Work?

For proof-of-work blockchains, this technology consists of three important concepts: blocks, nodes and miners.

What Is a Block?

Every chain consists of multiple blocks and each block has three basic elements:

- The data in the block.

- The nonce — “number used only once.” A nonce in blockchain is a whole number that’s randomly generated when a block is created, which then generates a block header hash.

- The hash — a hash in blockchain is a number permanently attached to the nonce. For Bitcoin hashes, these values must start with a huge number of zeroes (i.e., be extremely small).

When the first block of a chain is created, a nonce generates the cryptographic hash. The data in the block is considered signed and forever tied to the nonce and hash unless it is mined.

What Is a Miner in Blockchain?

Miners create new blocks on the chain through a process called mining.

In a blockchain every block has its own unique nonce and hash, but also references the hash of the previous block in the chain, so mining a block isn't easy, especially on large chains.

Miners use special software to solve the incredibly complex math problem of finding a nonce that generates an accepted hash. Because the nonce is only 32 bits and the hash is 256, there are roughly four billion possible nonce-hash combinations that must be mined before the right one is found. When that happens miners are said to have found the "golden nonce" and their block is added to the chain.

Making a change to any block earlier in the chain requires re-mining not just the block with the change, but all of the blocks that come after. This is why it's extremely difficult to manipulate blockchain technology. Think of it as "safety in math" since finding golden nonces requires an enormous amount of time and computing power.

When a block is successfully mined, the change is accepted by all of the nodes on the network and the miner is rewarded financially.

The whole point of using a blockchain is to let people — in particular, people who don't trust one another — share valuable data in a secure, tamperproof way.

— MIT Technology Review

What Is Decentralization in Blockchain?

One of the most important concepts in blockchain technology is decentralization. No one computer or organization can own the chain. Instead, it is a distributed ledger via the nodes connected to the chain. Blockchain nodes can be any kind of electronic device that maintains copies of the chain and keeps the network functioning.

Every node has its own copy of the blockchain and the network must algorithmically approve any newly mined block for the chain to be updated, trusted and verified. Since blockchains are transparent, every action in the ledger can be easily checked and viewed, creating inherent blockchain security. Each participant is given a unique alphanumeric identification number that shows their transactions.

Combining public information with a system of checks-and-balances helps the blockchain maintain integrity and creates trust among users. Essentially, blockchains can be thought of as the scalability of trust via technology.

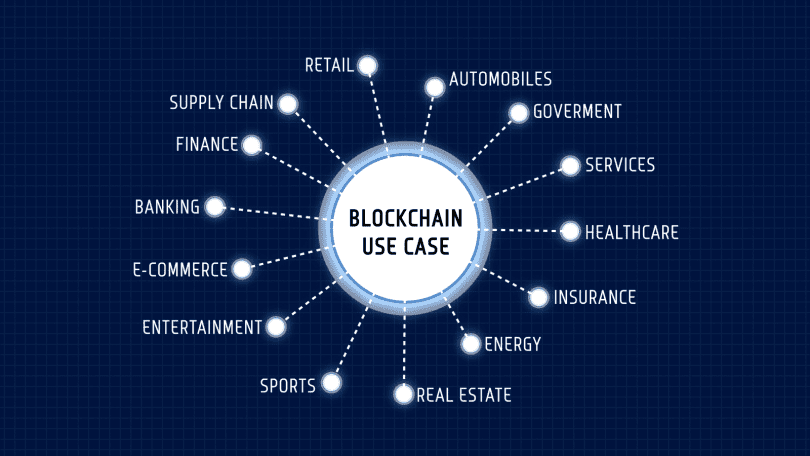

BLOCKCHAIN USES

Blockchain Applications

Blockchain isn’t only used for financial transactions. Due to its secure and transparent nature, the technology is versatile to needs beyond one area of expertise. Industries covering energy, logistics, education and more are utilizing the benefits of blockchain every day.

TOP BLOCKCHAIN USES & APPLICATIONS

- Cryptocurrency

- Cybersecurity

- Accounting and record keeping

- Supply chain

- Healthcare

Cryptocurrency: Blockchain vs Cryptocurrency

Blockchain’s most well-known use (and maybe most controversial) is in cryptocurrencies. Cryptocurrencies are digital currencies (or tokens), like Bitcoin, Ethereum or Litecoin, that can be used to buy goods and services. Just like a digital form of cash, crypto can be used to buy everything from your lunch to your next home. Unlike cash, crypto uses blockchain to act as both a public ledger and an enhanced cryptographic security system, so online transactions are always recorded and secured.

The term Bitcoin, for example, is used interchangeably to refer to both the blockchain and the cryptocurrency, but they remain as two separate entities. The very first blockchain application appeared in 2009 as Bitcoin, a crypto system using the distributed ledger technology. This also marked Bitcoin as the first “blockchain.” The aspect of blockchain being used to house this new digital currency is what brought both entities into association, and what led them quickly into the spotlight. The Bitcoin blockchain describes only the technology in which the currency is housed, while the Bitcoin cryptocurrency describes only the currency itself.

HOW DOES CRYPTOCURRENCY WORK?

Cryptocurrencies are digital currencies that use blockchain technology to record and secure every transaction. A cryptocurrency (Bitcoin, for example) can be used as a digital form of cash to pay for everyday items as well as larger purchases, like cars and homes. It can be bought using one of several digital wallets or trading platforms, then digitally transferred upon purchase of an item, with the blockchain recording the transaction and the new owner. The appeal of cryptocurrencies is that everything is recorded in a public ledger and secured using cryptography, making an irrefutable, timestamped and secure record of every payment.

To date, there are more than 20,000 cryptocurrencies in the world that have a total market cap around $1 trillion, with Bitcoin holding a majority of the value. These tokens have become incredibly popular over the last few years, with the value of one Bitcoin fluctuating between several thousands of dollars.

Here are some of the main reasons behind cryptocurrency’s recent popularity:

- Blockchain’s security makes theft much harder since each cryptocurrency has its own irrefutable identifiable number that is attached to one owner.

- Crypto reduces the need for individualized currencies and central banks. With blockchain, crypto can be sent to anywhere and anyone in the world without the need for currency exchanging or without interference from central banks.

- Cryptocurrencies can make some people rich. Speculators have been driving up the price of crypto, especially Bitcoin, helping some early adopters to become billionaires. Whether this is actually a positive has yet to be seen, as some retractors believe that speculators do not have the long-term benefits of crypto in mind.

- More and more large corporations came around to the idea of a blockchain-based digital currency for payments. In February 2021, Tesla announced that it would invest $1.5 billion into Bitcoin and accept it as payment for their cars.

Of course, there are many legitimate arguments against blockchain-based digital currencies. First, crypto isn’t a very regulated market. Many governments were quick to jump into crypto, but few have a staunch set of codified laws regarding it. Additionally, crypto is incredibly volatile due to speculators. Lack of stability has caused some people to get very rich, while a majority have still lost thousands of dollars.

Whether or not digital currencies are the future remains to be seen. For now, it seems as if blockchain’s meteoric rise is more starting to take root in reality than pure hype. Though it’s still making headway in this entirely-new, highly-exploratory field, blockchain is also showing promise beyond Bitcoin.

What Is a Blockchain Platform?

While a blockchain network describes the distributed ledger infrastructure, a blockchain platform describes a medium where users can interact with a blockchain and its network. Blockchain platforms are created to be scalable and act as extensions from an existing blockchain infrastructure, allowing information exchange and services to be powered directly from this framework.

An example of a blockchain platform includes Ethereum, a software platform which houses the Etherium, or ether, cryptocurrency. With the Ethereum platform, users can also create programmable tokens and smart contracts which are built directly upon the Ethereum blockchain infrastructure.

Beyond Bitcoin: Ethereum Blockchain

Originally created for Bitcoin to operate on, blockchain has long been associated with cryptocurrency, but the technology's transparency and security has seen growing adoption in a number of areas, much of which can be traced back to the development of the Ethereum blockchain.

In late 2013, Russian-Canadian developer Vitalik Buterin published a white paper that proposed a platform combining traditional blockchain functionality with one key difference: the execution of computer code. Thus, the Ethereum Project was born.

Today, the Ethereum blockchain lets developers create sophisticated programs that can communicate with one another through the blockchain itself.

Similarly to Bitcoin, it’s worth noting that the Ethereum blockchain and the Ethereum cryptocurrency are two separate entities.

Tokens

Ethereum programmers can create tokens to represent any kind of digital asset, track its ownership and execute its functionality according to a set of programming instructions.

Tokens can be music files, contracts, concert tickets or even a patient’s medical records. In the past couple of years, non-fungible tokens (NFTs) grew in popularity. NFTs are unique blockchain-based tokens that store digital media (like a video, music or art). Each NFT has the ability to verify authenticity, past history and sole ownership of the piece of digital media. NFTs have become wildly popular because they offer a new wave of digital creators the ability to buy and sell their creations, while getting proper credit and a fair share of profits.

Newfound uses for blockchain have broadened the potential of the ledger technology to permeate other sectors like media, government and identity security. Thousands of companies are currently researching and developing products and ecosystems that run entirely on the burgeoning technology.

Blockchain is challenging the current status quo of innovation by letting companies experiment with groundbreaking technology like peer-to-peer energy distribution or decentralized forms for news media. Much like the definition of blockchain, the uses for the ledger system will only evolve as technology evolves.

Smart Contracts

What is a smart contract? These are digital, programmed contracts that automatically enact or document relevant events when specific terms of agreement are met. Each contract is directly controlled through lines of code stored across a blockchain network. So once a contract is executed, agreement transactions become trackable and unchangeable. Though fundamental to the Ethereum platform, smart contracts can also be created and used on blockchain platforms like Bitcoin, Cardano, EOS.IO and Tezos.

Blockchain Applications for Industries

As mentioned, blockchain technology is being used far beyond just its roots in cryptocurrency — almost every modern industry is being morphed by the technology in some way.

Alongside banking and finance, blockchain is revolutionizing healthcare, record-keeping, smart contracts, supply chains and even voting. While the capabilities of such technology continue to grow, all the possible applications of blockchain are very much yet to be discovered.

BLOCKCHAIN HISTORY

Blockchain Evolution

The first concept of blockchain dates back to 1991, when the idea of a cryptographically secured chain of records, or blocks, was introduced by Stuart Haber and Wakefield Scott Stornetta. Two decades later the technology gained traction and widespread use. The year 2008 marked a pivotal point for blockchain, as Satoshi Nakamoto gave the technology an established model and planned application. The first blockchain and cryptocurrency officially launched in 2009, beginning the path of blockchain’s impact across the tech sphere.

2008

- Satoshi Nakamoto, a pseudonym for a person or group, publishes “Bitcoin: A Peer to Peer Electronic Cash System.”

2009

- The first successful Bitcoin (BTC) transaction occurs between computer scientist Hal Finney and the mysterious Satoshi Nakamoto.

2010

- Florida-based programmer Laszlo Hanycez completes the first ever purchase using Bitcoin — two Papa John’s pizzas. Hanycez transferred 10,000 BTCs, worth about $60 at the time.

- The market cap of Bitcoin officially exceeds $1 million.

2011

- 1 BTC = 1 USD, giving the cryptocurrency parity with the US dollar.

- Electronic Frontier Foundation, Wikileaks and other organizations start accepting Bitcoin as donations.

2012

- Blockchain and cryptocurrency are mentioned in popular television shows like The Good Wife, injecting blockchain into pop culture.

- Bitcoin Magazine launched by early Bitcoin developer Vitalik Buterin.

2013

- BTC market cap surpassed $1 billion.

- Bitcoin reached $100/BTC for the first time.

- Buterin publishes the “Ethereum Project” paper, suggesting that blockchain has other possibilities besides Bitcoin (like smart contracts).

2014

- Companies Zynga, The D Las Vegas Hotel and Overstock.com all start accepting Bitcoin as payment.

- Buterin’s Ethereum Project is crowdfunded via an Initial Coin Offering (ICO) raising over $18 million in BTC and opening up new avenues for blockchain.

- R3, a group of over 200 blockchain firms, is formed to discover new ways blockchain can be implemented in technology.

- PayPal announces Bitcoin integration.

- The first-known NFT is minted

2015

- Number of merchants accepting BTC exceeds 100,000.

- NASDAQ and San-Francisco blockchain company Chain team up to test the technology for trading shares in private companies.

2016

- Tech giant IBM announces a blockchain strategy for cloud-based business solutions.

- The government of Japan recognizes the legitimacy of blockchain and cryptocurrencies.

2017

- Bitcoin reaches $1,000/BTC for the first time.

- Cryptocurrency market cap reaches $150 billion.

- JP Morgan CEO Jamie Dimon says he believes in blockchain as a future technology, giving the ledger system a vote-of-confidence from Wall Street.

- Bitcoin reaches its all-time high at $19,783.21/BTC.

- Dubai announces its government will be blockchain-powered by 2020.

2018

- Facebook commits to starting a blockchain group and also hints at the possibility of creating its own cryptocurrency.

- IBM develops a blockchain-based banking platform with large banks like Citi and Barclays signing on.

2019

- China’s President Ji Xinping publicly embraces blockchain as China’s central bank announces it is working on its own cryptocurrency.

- Twitter & Square CEO Jack Dorsey announces that Square will be hiring blockchain engineers to work on the company’s future crypto plans.

- The New York Stock Exchange (NYSE) announces the creation of Bakkt - a digital wallet company that includes crypto trading.

2020

- BTC almost reaches $30,000 by the end of 2020.

- PayPal announces it will allow users to buy, sell and hold cryptocurrencies.

- The Bahamas becomes the world’s first country to launch its central bank digital currency, fittingly known as the “Sand Dollar.”

- Blockchain becomes a key player in the fight against COVID-19, mainly for securely storing medical research data and patient information.

2021

- Bitcoin surpasses $1 trillion in market value for the first time.

- Popularity for the implementation of Web3 rises.

- El Salvador becomes first nation to adopt Bitcoin as legal tender.

- Tesla buys $1.5 billion in BTC, becoming the first car manufacturer to accept Bitcoin as a form of automobile payment.

- The metaverse, a virtual environment incorporating blockchain technology, garners mainstream attention.

2022

- Cryptocurrency loses $2 trillion in market value, due to economic inflation and rising interest rates.

- Google launches a dedicated Digital Assets Team to provide customer support on blockchain-based platforms.

- The U.K. government proposes safeguards for stablecoin holders.

- Popular video game Minecraft bans blockchain technologies and NFT use in its game.